June 2026

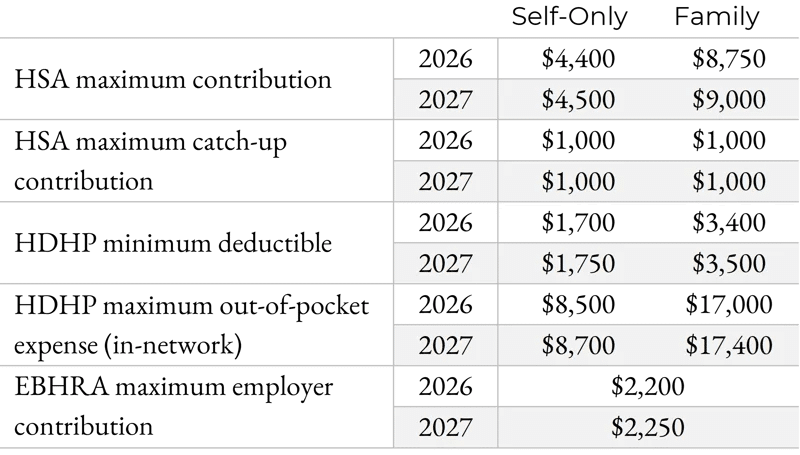

The IRS recently issued Revenue Procedure 2026-24, announcing the 2027 inflation-adjusted amounts for health savings accounts (HSAs), excepted benefit health reimbursement arrangements (EBHRAs), and high-deductible health plans (HDHPs). The newly announced figures result in increases in the applicable limits for 2027, including the maximum contribution limit for an HSA, the maximum amount that can be made newly available in an EBHRA, the minimum permissible deductible for an HDHP, and the maximum limit on out-of-pocket expenses for in-network services (e.g., deductibles, copayments, and other amounts aside from premiums) for qualifying HDHPs. These limits will differ depending on whether an individual is covered by a self-only or family coverage tier under an HDHP. The maximum permitted catch-up HSA contribution for eligible individuals who are 55 or older at any time during 2027 is not inflation-adjusted and remains unchanged for 2027.

HSAs and HDHPs

HSAs are tax-favored accounts that eligible individuals may use to pay qualified medical expenses. To be eligible to contribute to an HSA, an individual generally must be covered by an HSA-compatible HDHP and must not have disqualifying non-HDHP coverage.

The higher HSA contribution limit and HDHP out-of-pocket maximum will take effect January 1, 2027. The higher HDHP deductible limits will apply to plan years beginning on or after January 1, 2027.

EBHRAs

An EBHRA is a limited form of health reimbursement arrangement that may be offered as an excepted benefit if applicable requirements are satisfied. Because EBHRAs are subject to a separate annual limit, employers that sponsor EBHRAs should review plan documents, enrollment materials, and vendor communications to confirm that the 2027 amount is correctly implemented.

Employers that sponsor HDHPs and EBHRAs may need to make plan design changes as they are focusing on 2027 planning. Additionally, affected employers will need to ensure that they update all plan communications, open enrollment materials, and other documentation that addresses these limits to be sure participants and beneficiaries are adequately informed.

Employer Action Items

- Confirm that any HDHP offered for the 2027 plan year satisfies the increased minimum deductible requirements and does not exceed the applicable maximum out-of-pocket limits for self-only and family coverage.

- Work with payroll providers, HSA custodians, and benefits administrators to ensure that the 2027 HSA contribution limits are properly accounted for and communicated before the start of the 2027 plan year.

- Update summary plan descriptions, open enrollment materials, employee handbooks, benefits guides, and other participant-facing communications to reflect the new HSA, HDHP, and EBHRA limits.

- Employers sponsoring EBHRAs should review plan documents, reimbursement platforms, and vendor administration processes to ensure the 2027 maximum employer contribution limit of $2,250 is accurately implemented.